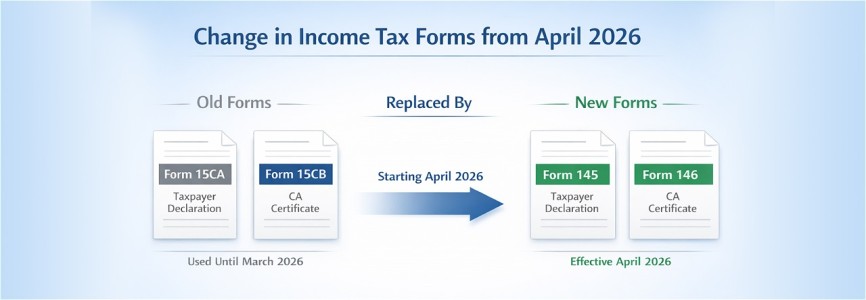

Imagine you are running a business in India, and one day you need to send money to someone outside the country, maybe a consultant, a vendor, or a service provider. Earlier, you were used to filing Forms 15CA and 15CB. Everything was familiar.

But suddenly, from 1st April 2026, things change.

The government, through the Central Board of Direct Taxes (CBDT), introduces Income Tax Rules 2026, and now you must use Form 145 and Form 146 instead of the old forms.

At first glance, it may look like just a name change. But in reality, it is a major upgrade in the compliance system. These new forms are more structured, more digital, and designed to make tracking foreign payments easier and more transparent.

What Has Changed: Old Forms vs New Forms

Under the earlier system, Form 15CA was used as a declaration by the person making the payment, and Form 15CB was a certificate issued by a Chartered Accountant. Under the new system, Form 145 replaces Form 15CA, and Form 146 replaces Form 15CB.

The purpose of both sets of forms remains similar, but the structure, legal backing, and reporting process are now updated. The new system is more integrated and helps the tax department track foreign remittances more effectively.

What is Form 145 and Why is it Important

Form 145 is a declaration that must be filed before making any payment to a non-resident or a foreign company. This form tells the Income Tax Department that a payment is about to be made outside India.

Every person who is responsible for making such a payment must submit this form 145 before sending the money. This applies to businesses, professionals, and companies alike.

In simple terms, Form 145 acts like an intimation to the government. It provides details of the transaction, the parties involved, and whether the payment is taxable or not.

However, not every payment requires Form 145. There are certain exceptions. For example, if an individual is making a remittance under the Liberalised Remittance Scheme, or if the payment falls under certain RBI-approved categories, the form may not be required.

Understanding the Structure of Form 145

Form 145 is divided into four parts, and each part applies to a different situation.

-

Part A: When your payment is taxable but small (up to Rs.5 lakh)

-

Part B: When payment is large (above Rs.5 lakh) and you already have approval from the tax officer

-

Part C: When payment is large and you need a CA certificate (this is where Form 146 comes in)

-

Part D: When the payment is not taxable at all

This structure makes it easier to classify transactions based on their nature and value.

What is Form 146 and When is it Required

Form 146 is a certificate issued by a Chartered Accountant. It is required when the payment is taxable and exceeds Rs. 5 lakh, and the taxpayer has not taken approval from the Assessing Officer.

Form 146 is used to certify the taxability of the remittance. The Chartered Accountant checks whether the payment is taxable under Indian law and whether any benefit is available under international tax treaties.

In simple words, Form 146 is like a professional confirmation that the tax calculation and deduction are correct before the money is sent abroad.

Role of Chartered Accountant in Form 146

The Chartered Accountant plays an important role in this process. The CA examines the agreement, the nature of payment, and the applicable tax laws. The CA also checks provisions of Double Taxation Avoidance Agreements, if applicable.

After proper verification, the CA issues Form 146. This ensures that the remittance complies with all legal requirements and reduces the chances of errors.

Documents Required for Filing

To file Form 145 and Form 146, certain documents are required. These include invoices, agreements or contracts, details of the sender and receiver, and bank details. If tax treaty benefits are claimed, a Tax Residency Certificate is also needed.

Having these documents ready helps in smooth and accurate filing.

How to File Form 145 and Form 146

These forms can be filed online through the Income Tax e-filing portal. There is also an offline utility available, which allows users to prepare the form without internet and upload it later.

This offline method is especially useful for businesses that need to file multiple forms at once.

Timing and Compliance Requirements

There is no fixed due date for filing these forms. However, one important rule must always be followed. The forms must be submitted before making the remittance.

These are event-based forms, which means they must be filed for each transaction separately. There is no limit on how many times they can be filed in a year.

Penalties for Non-Compliance

Non-compliance with these forms can lead to serious consequences. If a person fails to file Form 145 or provides incorrect information, a penalty of up to Rs. 1 lakh may be imposed. Similarly, if a Chartered Accountant provides incorrect information in Form 146, a penalty of up to Rs. 10,000 per certificate may apply.

This makes it very important to ensure accuracy while filing.

Why Form 145 and Form 146 Are Important

These forms play a key role in the tax system. They help the government track foreign payments and ensure that proper tax is deducted. They also bring more transparency and reduce the chances of tax evasion. With increased digital integration, these forms also help in better risk analysis and verification by the tax department.

FAQs on Form 145 (Earlier Form 15CA)

Q1. What is Form 145?

Ans. Form 145 is a mandatory declaration that must be filed before making a payment to a non-resident or a foreign company.

Q2. Who should file Form 145?

Ans. Any person responsible for making a payment to a non-resident (not being a company) or to a foreign company must file Form 145 before remittance.

Q3. Who is exempt from filing Form 145?

Ans. Form 145 is not required in the following cases:

-

Remittance by an individual under Liberalised Remittance Scheme (LRS)

-

Remittance by an IFSC unit

-

Payments covered under specified RBI purpose codes

Q4. What is the time limit for filing Form 145?

There is no fixed time limit, but it must be filed before making the remittance.

Q5. How many times can Form 145 be filed?

Ans. There is no limit. It must be filed for each transaction (event-based).

Q6. Which part of Form 145 should be filled?

Ans.

-

Part A: Taxable payment up to Rs.5 lakh

-

Part B: Taxable payment above Rs.5 lakh with AO certificate

-

Part C: Taxable payment above Rs.5 lakh with CA certificate (Form 146)

-

Part D: Non-taxable payment

Q7. What documents are required for Form 145?

Ans.

-

Invoice or agreement

-

Remitter and remittee details

-

Bank details

-

AO or CA certificate (if applicable)

-

TRC and Form 41 (if claiming DTAA benefit)

Q8. How can Form 145 be filed?

Ans.

-

Online via e-filing portal

-

Offline using utility tool and later uploading

Q9. What is the offline utility?

Ans. It is a tool to prepare the form without internet and upload later, useful for bulk filing.

Q10. How to e-verify Form 145?

Ans.

-

Through Digital Signature Certificate (DSC)

-

Through Electronic Verification Code (EVC)

(DSC is mandatory for TAN users)

Q11. How to confirm successful submission?

Ans. An acknowledgement number and transaction ID are generated, and confirmation is sent via email and SMS.

Q12. When is Form 146 required?

Ans. When the payment is taxable, exceeds Rs.5 lakh, and no AO certificate is obtained.

Q13. Is PAN of the remittee mandatory?

Ans. No. If PAN is not available, TIN can be provided.

Q14. What is TIN?

Ans. TIN is a Taxpayer Identification Number used by the foreign country to identify the recipient.

Q15. Do I need to submit Form 145 to the bank?

Ans. Yes. A copy must be submitted to the authorised dealer bank before remittance.

Q16. Can Form 145 be edited after submission?

Ans. No, it cannot be edited.

Q17. Can Form 145 be withdrawn?

Ans. Yes, within 7 days of submission.

Q18. Does withdrawing Form 145 also withdraw Form 146?

Ans. Yes. If Part C is withdrawn, Form 146 is also automatically withdrawn.

Q19. What is UDIN and why is it important?

Ans. UDIN is a unique number generated by ICAI to verify authenticity of documents.

Q20. What is the outcome of Form 145?

Ans. The form is used by the tax department for verification, tracking, and risk analysis.

Q21. What are the penalties for non-compliance?

Ans. Failure or incorrect filing can lead to a penalty of up to Rs.1 lakh.

Q22. Why is Form 145 important?

Ans.

-

Tracks foreign remittances

-

Ensures proper tax deduction

-

Helps in compliance and verification

-

Supports risk analysis by tax authorities

FAQs on Form 146 (Earlier Form 15CB)

Q1. What is Form 146?

Ans. Form 146 is a Chartered Accountant certificate required when filing Part C of Form 145 for taxable remittances exceeding Rs.5 lakh.

Q2. Who can file Form 146?

Ans. Only a Chartered Accountant registered on the e-filing portal and assigned the form can file it.

Q3. Is Form 146 mandatory?

Ans. Yes, if:

-

Payment is taxable

-

Amount exceeds Rs.5 lakh

-

No AO certificate is obtained

Q4. What is the purpose of Form 146?

Ans. It certifies taxability of the remittance as per Income Tax Act and DTAA provisions.

Q5. How to assign Form 145 Part C to a CA?

Ans. Login → My Account → Add CA → Enter CA details → Select Form 146 → Submit

Q6. What are prerequisites for filing Form 146?

Ans.

-

CA must be registered on e-filing portal

-

DSC must be registered

-

Form must be assigned by taxpayer

Q7. What is the time limit for filing Form 146?

Ans. No fixed time limit, but it must be filed before filing Part C of Form 145.

Q8. How many times can Form 146 be filed?

Ans. No limit. It is filed per transaction.

Q9. What documents are required?

Ans.

-

Agreements and invoices

-

Remittance details

-

Bank details

-

TRC and Form 41 (if applicable)

Q10. How can Form 146 be filed?

Ans.

-

Online via portal

-

Offline via utility tool

Q11. What is offline utility?

Ans. A tool used for preparing forms offline and uploading later, useful for bulk filings.

Q12. How to e-verify Form 146?

Ans. Only through DSC of the Chartered Accountant.

Q13. How to confirm successful submission?

Ans. Acknowledgement number and confirmation via email/SMS.

Q14. Can Form 146 be edited after submission?

Ans. No, it cannot be edited.

Q15. Can Form 146 be withdrawn?

Ans. Yes, within 7 days, subject to conditions.

Q16. What is the outcome of Form 146?

Ans. It is used to prefill Part C of Form 145 and is marked “consumed” once used.

Q17. What is UDIN and why is it important?

Ans. UDIN ensures authenticity and can be verified through ICAI.

Q18. What are penalties for incorrect Form 146?

Ans. Penalty up to Rs.10,000 per certificate.

Q19. Why is Form 146 important?

Ans. It ensures that a qualified professional verifies taxability before funds are sent outside India.

Conclusion

The replacement of Forms 15CA and 15CB with Form 145 and Form 146 is an important step in modernising India’s tax system. While the change may seem confusing at first, the basic concept remains simple.

Form 145 is the declaration made by the taxpayer, and Form 146 is the certificate issued by the Chartered Accountant when required. Once this flow is understood, compliance becomes much easier.

Businesses and individuals dealing with foreign payments should understand these new forms carefully to avoid penalties and ensure smooth transactions. If you need Form 145 and Form 146, you can connect with us and our team will connect you with a Chartered Accountant who can help you in the same.

_crop10_thumb.jpg)

_for_FY_2025-26_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_Filing_Due_Dates_for_FY_2024-25_learn_crop10_thumb.jpeg)

_of_GST_Act_learn_crop10_thumb.jpg)

_Under_GST_learn_crop10_thumb.jpg)

_crop10_thumb.jpg)

_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_of_the_Income_Tax_Act_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_crop10_thumb.jpg)

_in_The_Income_Tax_Act,_1961_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_of_the_Income_Tax_Act_learn_crop10_thumb.jpg)

_Of_Income_Tax_Act_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_for_Import_and_Export_learn_crop10_thumb.jpg)

_crop10_thumb.jpg)