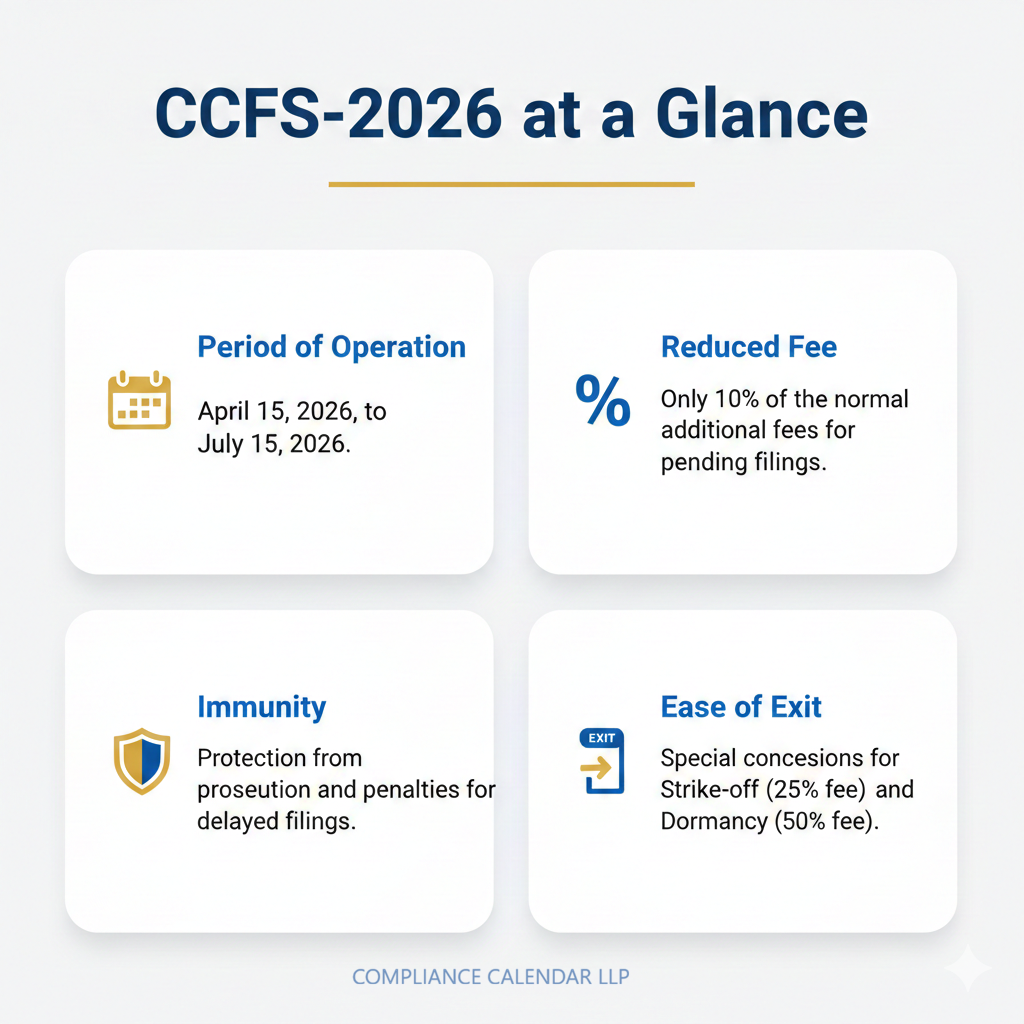

The Ministry of Corporate Affairs (MCA) has once again introduced a major compliance relief initiative for Indian companies. Through MCA General Circular No. 01/2026 dated 24 February 2026, the MCA has notified the Companies Compliance Facilitation Scheme, 2026 or CCFS-2026, a time-bound opportunity for companies to regularize pending annual filings at substantially reduced additional fees by 90% or to file dormant status of companies at half of the normal filing fees or to file STK-2 for fast track company closure at 25% fees INR 2,500 instead of INR 10,000.

This scheme comes at a time when lakhs of companies are burdened with heavy additional filing fees under the Companies Act, 2013. Since 1 July 2018, delayed filing attracts an additional fee of INR 100 per day without an upper limit for forms such as MGT-7 and AOC-4. For companies with multi-year defaults, this has resulted in penalties running into lakhs of rupees. CCFS-2026 provides a significant financial and compliance reset window.

This article by Compliance Calendar LLP explains everything about CFSS-2026, including eligibility, scheme benefits, immunity provisions, dormant option, strike-off, practical strategy, legal analysis, and FAQs.

Known MCA Settlement / Amnesty Schemes

The Ministry of Corporate Affairs (MCA) in India has introduced company-law settlement or compliance-relief schemes on multiple occasions over the past decade, generally to allow defaulting companies to regularise statutory filings with reduced fees and immunity from prosecution.

Below are 5 such schemes launched by MCA so far:

1. Company Law Settlement Scheme, 2010 (CLSS-2010)

First major amnesty scheme under the Companies Act, 1956.

2. Company Law Settlement Scheme, 2011 (CLSS-2011)

Extension / fresh window for defaulting companies.

3. Company Law Settlement Scheme, 2014 (CLSS-2014)

Introduced after the enforcement of the Companies Act, 2013, to regularise filings.

4. Companies Fresh Start Scheme, 2020 (CFSS-2020)

Covid-19 relief scheme allowing companies to file pending documents with immunity from penalty.

5. Companies Compliance Facilitation Scheme, 2026 (CCFS-2026)

Introduced vide General Circular No. 01/2026 dated 24 February 2026

The MCA has introduced formal company law settlement/compliance relief schemes four times earlier, notably in 2010, 2011, 2014, and in 2020 making CCFS-2026 as the fifth one. However, this is the first time that 75% waiver has been given in STK-2 fees making it INR 2,500 from regular filing fees of INR 10,000.

Note: It is important to note that earlier STK-2 filing fees were increased from INR 5,000 to INR 10,000.

Why was MCA CCFS-2026 Introduced?

Under the Companies Act, 2013; Section 92 mandates filing of Annual Return (MGT-7/MGT-7A) & Section 137 mandates filing of Financial Statements (AOC-4 series). Failure to file attracts:

-

Additional filing fees under the Companies (Registration Offices and Fees) Rules, 2014

-

Penalty proceedings

-

Adjudication under Section 454

-

Prosecution in certain cases

-

Director disqualification risks

-

DIN activation issues

-

Banking and funding restrictions

It is important to note that since 2018, the INR 100 per day additional fee structure has made default correction extremely expensive. Recognizing this burden, especially on MSMEs, startups, and inactive companies, MCA has introduced CCFS-2026 as a compliance regularisation scheme.

CCFS Scheme Period

Effective from 15 April 2026, and the last date is 15 July 2026. This is a 3-month one-time compliance window.

MCA Benefit: Only 10% of Additional Fees Payable

The biggest relief under CCFS-2026 is that they have been waived of 90% of the additional fees payable.

Companies can file pending annual return and financial statement forms by paying:

-

Normal filing fee, plus

-

Only 10% of the total additional fees are payable

Instead of paying 100% additional fee under the regular regime, the CFSS-2026 coupon gives you 90% discount.

Example Illustration

Suppose a company has an AOC-4 pending for 3 years and an additional fee calculated under the normal regime: Rs.1,50,000. Under CCFS-2026, the Company pays:

-

Normal filing fee

-

Only Rs.15,000 (10% of Rs. 1,50,000)

-

Savings: Rs. 1,35,000

For companies with long-pending filings, this is a massive financial relief.

Forms Covered Under CCFS-2026

The scheme covers “relevant e-forms” including:

Under the Companies Act, 2013: MGT-7, MGT-7A, AOC-4, AOC-4 CFS, AOC-4 XBRL, AOC-4 NBFC (Ind AS), ADT-1, FC-3 and FC-4

Under the Companies Act, 1956: Form 20B, Form 21A, Form 23AC, Form 23ACA, Form 66 and Form 23B

This ensures old defaults can also be corrected who did not take advantage of the earlier MCA Scheme.

Immunity from Penalties Under Sections 92 & 137

One of the most important features is that if companies complete pending filings during the scheme period, immunity is granted from:

-

Penalty under Section 92 (Annual Return)

-

Penalty under Section 137 (Financial Statements)

This reduces exposure to adjudication proceedings and monetary penalties.

Important: Immunity applies only if filings are completed within the scheme window.

Dormant Company Option Under Section 455

CCFS-2026 also provides strategic relief for inactive companies.

Companies may apply for Dormant status by:

-

Filing e-Form MSC-1

-

Paying only 50% of the normal filing fee

This is beneficial for:

-

Startups not yet operational

-

Holding companies

-

Asset holding companies

-

Companies preserving brand names

-

Investment SPVs

Dormant companies:

-

Remain on register

-

Face minimal compliance

-

Avoid heavy recurring penalties

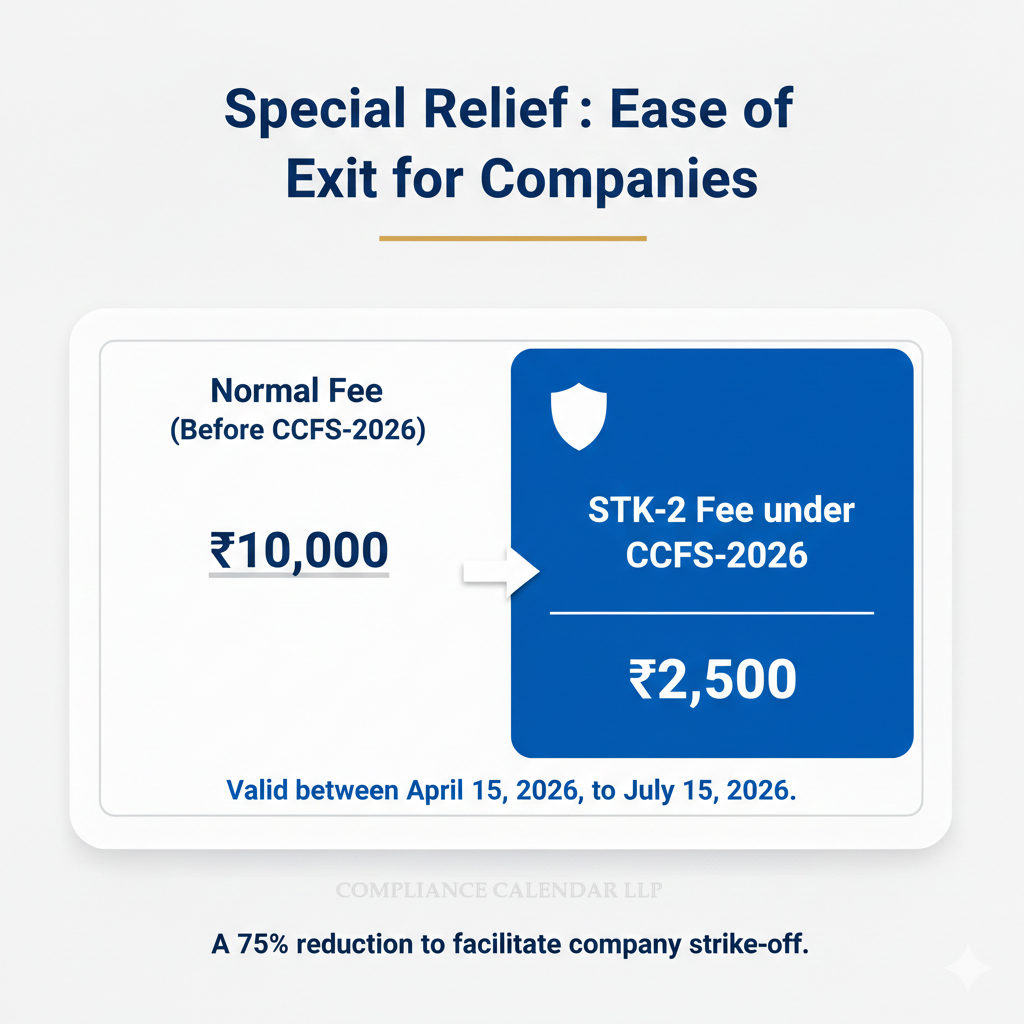

Strike Off Option at 25% Filing Fee

Companies that no longer wish to continue operations can:

-

File STK-2 during the scheme period

-

Pay only 25% (INR 2,500) of the actual filing fee of INR 10,000

This makes closure cheaper and faster, and is ideal for:

-

Inactive private companies

-

Failed startups

-

Non-operational MSMEs

Companies Not Eligible Under CCFS-2026

The scheme does NOT apply to:

-

Companies under final strike-off notice (Section 248)

-

Companies already applied for strike-off

-

Companies already declared Dormant before the scheme

-

Amalgamated companies

-

Vanishing companies

MCA has kept these exclusions to prevent misuse.

Legal Authority Behind the Scheme

The scheme is issued under powers conferred under:

-

Section 460 of the Companies Act, 2013 (condonation of delay)

-

Section 403 (additional fees)

-

Administrative Powers of the Central Government

Impact on Directors

Regularising filings:

-

Prevents further adjudication

-

Protects directors from penalty exposure

-

Reduces compliance red flags

-

Improves credit and banking credibility

Normal Regime Vs CCFS-2026

|

Particular |

Normal Regime |

CCFS-2026 |

|

Additional Fees |

INR 100 per day |

Only 10% of total |

|

Penalty Exposure |

Applicable |

Immunity available |

|

Dormant Fee |

100% normal |

50% |

|

STK-2 Fee |

100% |

25% |

|

Window |

Continuous |

15 Apr – 15 Jul 2026 |

How to Take Advantage of CCFS-2026

Step 1: Conduct compliance status review

Step 2: Calculate additional fee exposure

Step 3: Prepare pending financial statements

Step 4: Conduct board meeting approvals

Step 5: File AOC-4 and MGT-7

Step 6: Apply for Dormant or Strike-off if required

Time is limited under CFSS-2026 as it is valid only between April 15 to July 15 in 2026, making the total number of available days to 92, unless MCA further extends CFSS-2026 beyond July 15, 2026.

Conclusion

Companies should immediately review their compliance status and plan filings within the CFSS-2026 period. Do not wait until July 15, 2026, as last-minute filings may lead to technical issues or missed deadlines. This is a valuable opportunity to complete pending filings at significantly reduced additional fees with MCA.

For professional assistance, write to info@ccoffice.in or connect with us at 9988424211 via Call or WhatsApp.

FAQs on Companies Compliance Facilitation Scheme, 2026 (CCFS-2026)

1. What is the Companies Compliance Facilitation Scheme, 2026?

The Companies Compliance Facilitation Scheme, 2026 (CCFS-2026) is a one-time relief scheme introduced by the Ministry of Corporate Affairs to allow companies to file pending annual returns and financial statements at a substantially reduced additional fee and obtain immunity from penalty proceedings under specific provisions of the Companies Act, 2013.

2. When does the CCFS-2026 Scheme come into force?

The Scheme is effective from 15 April 2026 and will remain in force until 15 July 2026. This means companies have a 3-month window (92 days in total) to regularise pending filings.

3. What is the objective of this Scheme?

The Scheme aims to:

-

Provide relief to companies burdened with heavy additional filing fees.

-

Improve overall compliance levels.

-

Ensure that MCA registry reflects updated and accurate data.

-

Facilitate inactive companies to opt for dormancy or strike off at concessional fees.

4. What filings are covered under the Scheme?

The Scheme covers various pending annual and related filings, including:

Under Companies Act, 2013:

-

MGT-7 / MGT-7A (Annual Return)

-

AOC-4 (Financial Statements)

-

AOC-4 CFS

-

AOC-4 NBFC (Ind AS)

-

AOC-4 XBRL

-

ADT-1

-

FC-3, FC-4

Under Companies Act, 1956:

-

Form 20B

-

Form 21A

-

Form 23AC / 23ACA

-

23AC-XBRL / 23ACA-XBRL

-

Form 66

-

Form 23B

5. What is the reduced fee structure under CCFS-2026?

Under the Scheme:

-

Normal filing fees – Payable as per prescribed rules.

-

Additional fees – Only 10% of the total additional fees payable under normal provisions.

This provides massive financial relief where additional fees had accumulated without upper limit.

6. Is there any benefit for dormant company status?

Yes. Companies may apply for Dormant Status under Section 455 by filing Form MSC-1 and pay only 50% of the normal filing fee. This is particularly beneficial for inactive companies wishing to retain corporate status with minimal compliance.

7. Is strike-off also allowed at concessional fees?

Yes. Companies may apply for strike-off by filing Form STK-2 during the Scheme period by paying only 25% of the applicable filing fees.

8. Does the Scheme provide immunity from penalty?

Yes, immunity is granted in specific cases.

Where filings are made under the Scheme:

-

Proceedings under Section 92 (Annual Return) and

-

Section 137 (Financial Statements)

shall be concluded and no penalty shall be levied, subject to conditions mentioned in the circular.

9. Are there any conditions for immunity?

Immunity is available only if:

-

Filing is done before issuance of adjudication notice; or

-

Filing is completed within 30 days of issuance of notice; and

-

No prosecution has already been initiated (for certain forms).

If adjudication order imposing penalty has already been passed, liability to pay penalty continues.

10. Which companies are NOT eligible for the Scheme?

The Scheme does not apply to:

-

Companies against which final strike-off notice under Section 248 has already been initiated.

-

Companies that have already filed application for strike-off.

-

Companies that have already applied for dormant status before Scheme inception.

-

Companies dissolved pursuant to amalgamation.

-

Vanishing companies

11. Is this Scheme automatic or application-based?

There is no separate application for immunity. Relief is granted automatically upon filing eligible forms within the Scheme period and complying with the prescribed conditions.

12. What happens after 15 July 2026?

After the conclusion of the Scheme:

-

Registrars of Companies will initiate necessary action against companies that have not availed the Scheme.

-

Normal additional fees and penalty proceedings will apply.

-

Non-compliant companies may face adjudication or strike-off proceedings.

13. Does the Scheme waive normal filing fees?

No. Normal filing fees remain payable. Only the additional fees are reduced to 10%.

14. Can a company avail the Scheme for multiple financial years?

Yes. All pending filings due for any previous financial year can be filed during the Scheme window, provided they fall under covered forms.

15. Why should companies not wait until the last date?

-

Technical glitches on MCA portal are common near deadlines.

-

Professional certification may require time.

-

Digital signature validity issues may arise.

-

Large additional fees relief is time-bound.

-

Early compliance ensures smooth closure of defaults.

_crop10_thumb.jpg)

_crop10_thumb.jpg)

_crop10_thumb.jpg)

_crop10_thumb.jpg)

_crop10_thumb.jpg)

_crop10_thumb.jpg)

_crop10_thumb.jpg)

-suratgujarat-section-158_crop10_thumb.jpg)

-suratgujarat_crop10_thumb.jpg)

-(33)_crop10_thumb.jpg)

-ahmedabad_crop10_thumb.jpg)

-learn_crop10_thumb.jpg)

-learnn_crop10_thumb.jpg)

_crop10_thumb.jpg)

_Guidelines_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_crop10_thumb.jpeg)

_crop10_thumb.jpg)

_Second_Amendment_Rules,_2025_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpeg)

_learn_crop10_thumb.jpg)

_rd_roc_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_Learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_learn_crop10_thumb.jpg)

_crop10_thumb.jpeg)

_crop10_thumb.jpg)